6 Points of Margin Analysis

Margin Management

Controlling margin is key….

changing supplier product lines and costs,

expansion of on-site OH&S requirements

-

a challenging market

….. all emphasise the importance of margin review.

Most Australian builders understand this importance, but fail to implement systems to properly control the operational and financial processes, making it difficult to fully understand where margin is repeatedly being lost.

When margin erosion is identified and tracked, businesses are able to take advantage of the information and explore possibilities to compete in a tightening market.

This paper examines the six points throughout the building cycle where margin should be examined. By reviewing the expected margin at each of these points, processes can be implemented to take required corrective action to prevent recurring margin erosion.

These controls should commence when tendering and finish at job completion encompassing:

Pricing and Costs

Tender Production

Contract Issue

Site Start

Handover

Job Completion

6 Points Overview

Area Pricebook |

Standard Bills of Materials should be used to determine costs and recommended pricing. Pricing information can be recorded by Area and Effective Date enabling the control of Pricing, Costs and expected Margin. |

Tender Preparation |

Tenders can be produced consistently based on Area Pricebook whilst still allowing for non-standard items using Supplier Rates that can also be managing using Areas and Effective Dates. |

Contract Issue |

Contract produced and issued for signing. Margin carried over from Tender. Job specific quantities are completed including updates from colour selections. Purchase Orders created based no tender, issued and emailed to suppliers with necessary attachments. |

Site Start |

Site Work started. Anticipated margin declared so that any additional costs impacting margin are tracking using Extra to Schedule (ETS) controls. |

Handover |

Handover of project to customer. Current Margin can be compared to original anticipated margin with reasons for margin erosion examined. |

Job Completion |

Final margin determined. Can be compared to original anticipated margin with reasons for margin erosion examined. |

Area Pricebook

Having structured product release processes and procedures is vital for the consistent creation of bills of materials. Bills are the key facet to determining expected costs, prices and margins.

Ensuring complete margin control throughout the entire building cycle starts with correct margins at the time of product release. There are few gains in tracking a low margin during construction if the source of the problem is the price book.

Builders need the ability to report based on a number of different costing options to provide the most competitive price available. BusinessCraft achieves this through the BusinessCraft Cost Comparison report providing cost centre summaries based on:

Different Pricing Areas

Different Effective Dates

Average, Minimum or Maximum Costs

Many of the problems faced when tracking margins, is the disconnection that exists between systems. An integrated system ensures that the authorised costs and prices released flow through the various system processes which typically cannot be achieved by separate systems.

The control of costs and prices within BusinessCraft ensures that expected margins are transferred through to the tender and contract stages.

Tender Preparation and Contract Issue

Margin management during tender preparation can be difficult without appropriate integrated systems in place.

For example, in many cases costs are in the Purchasing system, and prices are in the Sales or Estimating system. This lack of integration causes a disconnect between costs and prices and in turn the inability to properly control and track margin.

However, an integrated system, such as BusinessCraft does not have this problem with accurate sell prices and costs. This enables expected margin to be checked if margin erosion occurs later in the building cycle.

Because the standard bills can be used as the basis for a tender, tender specific changes can be made to bill quantities, with BusinessCraft recalculating costs to determine expected margin for that tender.

Site Start

Any analysis of the expected job margin after site start needs to have a solid starting point. This is why it is vital to have accurate estimated quantities that are costed prior to commencing on site.

For some builders, this is not always possible, however an anticipated budget is usually known prior to commencement on site.

Many builders do not record what the expected margin is at job completion, so how can their systems accurately tell them when the margin erosion is occurring.

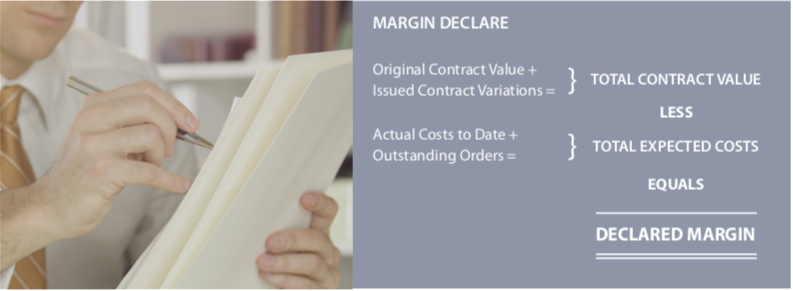

The margin declaration process in BusinessCraft delivers this by locking in the ‘declared’ (or expected) margin prior to commencing on site. Typically, all purchase orders would be raised by this point, or an expected budget known.

Once this margin is declared, BusinessCraft is able to track any erosion in the margin by utilising the integrated Extra to Schedule (ETS) capabilities. This ensures that a complete history is recorded for any cost-overruns that occur throughout the construction stages, allowing for comparison between the declared margin and the current job margin.

Handover

Typically, margins are continually changing throughout construction, and calculating work in progress should be an easy task. But, many builders spend a considerable amount of time on this, which shouldn’t be the case.

BusinessCraft’s configurable turnover calculation works can be used during construction to report on recommended revenue and cost take-ups creating the necessary journals to keep financial records up-to-date and accurate.

When construction has been completed, an analysis can be carried out to check expected margin. It is still not possible at this stage to determine final margin, as invoices are still being received from suppliers and subcontractors well after construction has finished.

It is important to include required outstanding orders in margin calculations, but also to exclude outstanding purchase orders that are no longer required or will incur no further cost. By doing this, a more accurate anticipated job margin can be determined.

Job Completion

The service and warranty period has completed and all costs should by now be received. This is now the stage when final job margin can be reviewed. The Job Costing Detail report provides a summary of all of the costs, including cost-overruns with the reason for each, resulting in a complete picture for the project.

Summary

One of the key drivers of your success is your ability to understanding the margins that your projects are achieving. With the market in the building industry consistently changing with varying economic factors, new players entering the market and the many suppliers constantly changing their products and rates, producing good quality products and services cannot be the only key driver for success.

By implementing integrated, efficient business systems and processes, your company can gain the flexibility, integration and control to respond quickly to market changes. Whether a new supplier is offering better products and rates or an aggressive competitor moves into a region that you have long dominated, you need flexible processes and systems in place to respond quickly and efficiently.

BusinessCraft’s fully integrated corporate management solution provides the complete margin analysis tool, by enabling 6 key steps of margin review. From financials to contract management and ordering, BusinessCraft provides the control and industry understanding that assists in achieving your business objectives.

Revision 1

30th December 2019